Executive Summary

Automotive aftermarket distributors must pivot from hardware vendors to “Systems Integrators” to survive a market shift in which software control outweighs physical inventory. Success is no longer defined by traditional sales volume, but by digital velocity, specifically maintaining sub-100ms API speeds for AI-driven ordering, securing digital “tokens” for encrypted vehicle calibrations, and eliminating “phantom inventory” through real-time data synchronization. As the industry moves toward a bimodal fleet of aging ICE vehicles and new EVs, leaders will be those who capture the total household service spend and shift their revenue mix toward high-margin digital subscriptions rather than one-off component sales.

Key Takeaways

To thrive, leaders must pivot from high-volume hardware distribution to high-velocity digital integration.

- The 100ms Speed Rule: In a world of automated ordering, speed is your best salesperson. Every 0.1-second delay in your digital system costs you 1% in sales because automated buyers will simply skip “slow” data for a faster competitor.

- The “Software Handshake”: Selling hardware isn’t enough anymore. Modern parts (such as smart sensors) require a digital “key” to be activated. If you don’t provide the software token to authenticate the part, 47% of shops will reject the repair.

- Real-Time Inventory or Bust: Shops can’t afford to lose a bay to “Phantom Inventory” – parts that show as “in-stock” online but aren’t on the shelf. Total accuracy and instant updates are now the gold standard for shop productivity.

- The Hybrid Household: Most families now own both a gas vehicle and an EV. To keep their business, you must use your steady revenue from traditional parts to fund the high-tech diagnostic tools needed to service their electric cars.

- The Shift to Services: By 2035, more than half of industry revenue will come from digital subscriptions and data services rather than metal parts. Companies that sell only physical products will see their long-term market value collapse.

The 2026 B2B Buyer: From Parts-Seekers to Data-Drivers

A distributor’s value is no longer just the physical inventory on the shelf. For the modern automotive aftermarket B2B buyer, data accuracy is as critical as the part itself. Today’s B2B buyers want it fast, easy, and self-service. Success comes down to one thing: delivering the right part, at the right time, backed by the right data. To dominate the market, you must solve the specific “pain points” of these four core segments:

- The Efficiency-First Service Center: The independent aftermarket cares about bay uptime. Every minute a car sits on a lift waiting for a part is lost revenue. They need instant Vehicle Identification Number (VIN) lookups and “Amazon-simple” reordering to get cars back on the road.

- The Uptime-Critical Fleet Operator: They care about predictability. Managing hundreds of rental or utility vehicles requires real-time stock visibility and bulk-ordering tools to hit tight service windows without fail.

- The High-Spec Technical Specialist: The speciality shops care about precision. Whether it’s a custom engine rebuild or a suspension upgrade, these experts need deep technical specs and highly specific part variants that standard catalogs often miss.

- The Macro-Scale Distribution Network: They care about scale. Managing massive inventory across regions requires “command and control” features, like custom pricing for specific branches and complex routing to ensure the closest warehouse fulfills the order.

The global automotive eCommerce market size was valued at USD 116.24 billion in 2025. The market is projected to grow from USD 135.14 billion in 2026 to USD 440.83 billion by 2034, exhibiting a CAGR of 15.93% during the forecast period. Fortune Business Insights

The 5 eCommerce Metrics That Define the New Aftermarket

The metrics that defined automotive eCommerce success for the last decade (Average Order Value (AOV), traffic, and gross margin) are rapidly becoming lagging indicators of a dying model. As the automotive aftermarket faces a ‘Triple Convergence’ of secure vehicle gateways and a bimodal fleet demographic, traditional aftermarket eCommerce metrics are no longer sufficient. To scale, organizations must adopt a more rigorous set of B2B eCommerce KPIs for automotive distribution.

With the average age of vehicles across mature markets hitting record highs – 12.8 years in the US, with the EU fleet average also trending above 12.5 years – and the rise of Software-Defined Vehicles (SDVs) creating a “Calibration Paywall,” profit will no longer be governed by who owns the inventory, but by who controls the digital permissions to install it. To survive the transition from “Parts Seller” to “Systems Integrator,” businesses must audit their setup against five new critical metrics measuring data velocity, integration reliability, and revenue quality.

1. API Response Speed (The “Latency” Rule)

In an AI-driven procurement environment, your primary customer may not be a human service advisor, but an autonomous AI agent querying your API for stock and pricing – your website is no longer just for humans. If your system takes longer than 100ms to respond to an automated query, you will be invisible to autonomous agents and large-scale fleet systems that will dominate 2026 purchasing. Speed isn’t a feature; it is your primary product.

- The Insight: Consumer loyalty has been replaced by sub-second certainty. Research from Amazon and Google confirms that every 100 milliseconds of latency costs approximately 1% in sales. If your API takes seconds to respond, you are effectively “offline” to the automated supply chains of the future.

- The Metric: Does your infrastructure allow for “Agent-ready” queries with 100% accuracy in under 100ms?

- Strategic Implication: You must decouple your front-end experience from legacy enterprise resource planning (ERP) systems using a Headless/Composable Architecture. Modernizing architecture to reduce page loads to under 2 seconds can drive a 42% surge in monthly order value.

2. Digital Repair Success Rate (The “Software” Metric)

As original equipment manufacturers ( OEMs) transition to zonal architectures and encrypted gateways, the independent aftermarket faces a “Calibration Paywall.” Selling the physical part is now only half the job. Vehicles are now software-defined, and distributors must track how often they successfully provide the digital “handshake” or token required to calibrate and finish the repair. If the shop can’t calibrate it, you haven’t sold a finished product.

- The Insights: A physical part cannot be installed without a digital key. Currently, 47% of workshops report having to turn down ADAS-related repairs due to insufficient digital capabilities.

- The Metric: Track the ratio of hardware sales to successful remote authentications. If you sell a radar sensor but cannot facilitate the digital handshake to calibrate it, you are selling an unfinished product.

- Strategic Implication: Distributors must evolve into “Digital Gatekeepers.” Success requires building proprietary technical help desks that aggregate these digital keys and “tokens” to ensure the shop can complete the repair both physically and digitally.

3. Inventory Accuracy (The “Phantom” Metric)

Body shops and repair centres are demanding “Just-in-Time” orchestration to maximize bay uptime, driven by the “Install-It-For-Me” (IIFM) phenomenon. Eliminating “Phantom Inventory” – parts that appear in stock but are physically unavailable due to data delays – is the new measure of supply chain integrity. Success is measured by your Soft-Allocation Speed, or how fast you can “lock” a part for a customer. Data latency in the warehouse kills shop bay productivity.

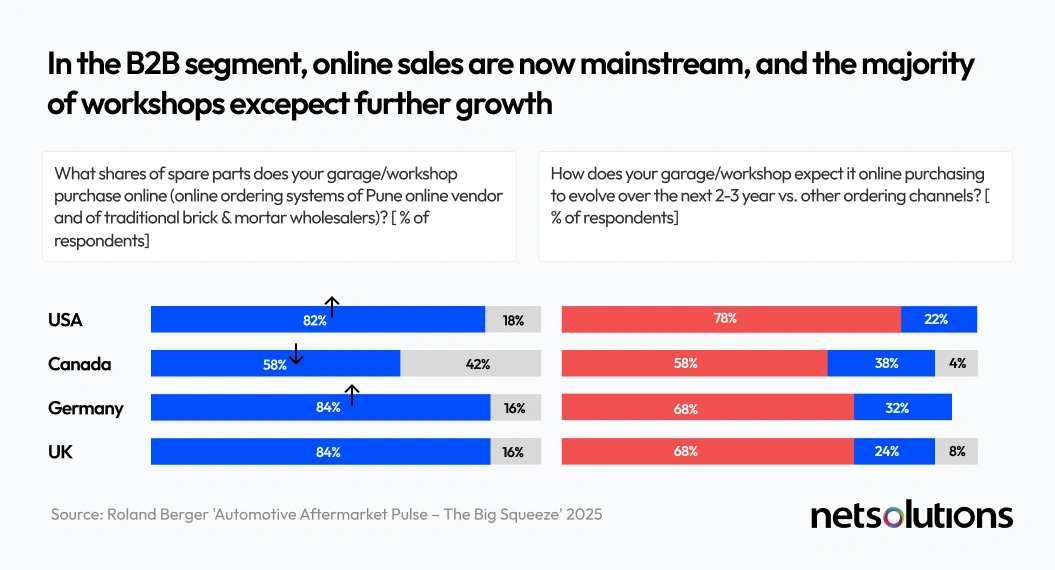

- The Insight: 92% of workshops now purchase significant volumes online and demand predictive availability and an assured delivery timeline. The leading friction point is “Phantom Inventory” – parts that appear “In Stock” but are unavailable due to batch-update delays between the warehouse and the webstore.

- The Metric: Measure Soft-Allocation Speed for Inventory. Can your system reserve stock at the moment of the quote (pre-booking) rather than at the moment of settlement?

- Strategic Implication: Move to API-driven “Logistics-as-a-Service.” Real-time synchronization eliminates the “Parts Tetris” mechanics play and ensures high first-contact resolution rates.

4. Household Revenue Share (The “Bimodal” Metric)

The global vehicle fleet is not just transitioning; it is bifurcating into a high-stakes “Hybrid Bridge.” While legacy ICE vehicles hit record average ages, Ford’s 2026 strategic pivot – prioritizing Extended-Range Electric Vehicles (EREVs) and hybrids over pure BEVs – signals a decade of “Triple-Complexity” platforms. By 2030, Ford expects 50% of its global volume to feature these multi-energy powertrains. Success is no longer about picking a side (ICE vs. EV); it is about capturing the entire household’s total service spend across all engine types.

- The Insight: We are in a “Great Divergence.” While software-related aftermarket services are surging at a 31.2% CAGR, traditional hardware revenue is stagnating. The 2026 market demands a “Hardware-Software Symbiosis” where diagnosing cell-level battery degradation is as routine as an oil change. Yet, the independent aftermarket is stalling: 25% of general repair shops currently refuse EV/Hybrid work due to a lack of specialized high-voltage training and equipment.

- The Metric: Household Share of Wallet. Are you capturing the high-margin ICE repairs, the hybrid generator maintenance, and the EV diagnostic events for the same household?

- Strategic Implication: If you cannot facilitate the “Software Handshake” for a hybrid’s generator or the battery health check for an EREV, you risk losing the high-volume maintenance revenue from the family’s secondary ICE vehicle. Use legacy ICE volume to subsidize the heavy CAPEX required for the high-voltage “Clean Room” facilities and diagnostic subscriptions needed to bypass the OEM “Calibration Paywalls.”

5. Digital Revenue Mix (The “Valuation” Metric)

Private Equity and institutional investors are shifting valuations away from companies based solely on hardware volume. Investors are re-rating the automotive sector based on the quality of earnings. While volume was the old standard, the most critical B2B eCommerce KPIs automotive firms now track revolve around the ratio of digital services to hardware sales. This shift in aftermarket eCommerce metrics reflects a move toward “data sovereignty.”

- The Insight: IBM research indicates that industry executives expect 51% of revenue to come from recurring digital sources (subscriptions, OTA updates, remote diagnostics) by 2035, up from just 15% today.

- The Metric: Recurring Revenue Mix. What percentage of your growth comes from “Uptime Subscriptions” or data monetization versus one-off, transactional part sales?

- Strategic Implication: Companies trapped in a hardware-only model will see their valuation multipliers collapse. The winners will be those who achieve “Data Sovereignty”, selling vehicle “uptime” outcomes rather than individual components.

Beyond Survival: How to Lead the Automotive Aftermarket

To lead the global automotive aftermarket, organizations must move beyond operational efficiency toward Systemic Sovereignty, a state where the distributor, not the manufacturer, controls the repair outcome.

Here is the strategic breakdown of that transition:

The Shift to Systemic Sovereignty

- Redefining the “Part”: Success requires viewing every physical component as a “digital-physical bundle.” If your fulfillment model relies on an OEM’s permission to calibrate a sensor, you are merely a vendor; true Orchestrators own the diagnostic path.

- Bypassing “Walled Gardens”: Survival in 2026 depends on creating independent diagnostic standards that ensure your SKU count and service capabilities evolve as rapidly as battery chemistry and ADAS technology.

- High-Performance Alliances: Market dominance belongs to those who transform fragmented workshop networks into a unified alliance. This means using digital tools to lower the shop’s total cost of service, not just selling them an individual component.

- Frictionless Complexity: The ultimate metric for 2026 is the “Automated Click.” You must reduce sophisticated software handshakes and encrypted gateway bypasses into a single, trusted action that even the most traditional technician can execute with confidence.

- Mastering the Digital Flow: The future of the B2B aftermarket is no longer about “moving metal.” It is about mastering the synchronized flow of data and parts to meet the Zero-Latency demands of a software-defined industry.

The rules of competition in 2026 are converging. The distributors who act now – on data infrastructure, digital integration, and subscription revenue – will define the market. Those who wait will be disintermediated by it.

Where Does Your Business Stand on the 2026 Readiness Curve?

The five metrics in this article aren’t predictions; they’re the new baseline. Take our free AI Readiness Assessment to find out how your current eCommerce infrastructure measures up, where your biggest gaps are, and what to prioritise first.

Frequently Asked Questions

The “call-in” model is receding. Leading online aftermarket sales (ECP in the European context, for example) have shifted to digital-first “Click & Collect.” More importantly, AI agents managing large fleets will bypass any distributor that cannot offer sub-second, machine-readable data.

Yes. A backorder is a supply chain failure; Phantom Inventory is a data latency failure. In an era where Velocity is the Product, selling a part you don’t actually have instantly erodes trust. Real-time API integration is the only fix.

It affects everything. Replacing a side mirror or a bumper now involves ADAS sensors that require a digital “handshake” to function. Without this token, the part is physically installed but digitally rejected by the vehicle’s gateway, leaving the car non-functional.